WeWork: A Strongly Profitable Business That Just Needs the Bananas to Ripen

Summary

While obscured by a tarnished reputation and suppressed pandemic-related occupancy rates, WeWork is a highly-profitable leader in a fast-growing industry

Flex coworking is the ideal product for businesses in a highly uncertain, post-pandemic world, and will continue to take share from commercial offices

WeWork offers a global footprint, unprecedent flexibility options, and a modern, premium work environment

Contrary to popular opinion, coworking spaces are strongly profitable businesses when occupancy is high. WeWork has high space efficiency and strong unit economics, and new management has massively cut costs

WeWork trades at just 6-7x 2023 EBITDA despite its strong growth prospects. Expect street to increase estimates and rerate the stock over time as occupancy recovers and sellside coverage grows

Look at WeWork with a Clean Slate

Much was made of WeWork’s failed IPO attempt in 2019 when the media piled onto Adam Neumann’s excesses and a seemingly questionable business model. After ending the IPO attempt and kicking Adam Neumann out, the general public moved on to the next tech laughingstock and forgot about WeWork.

During that forgotten time, new management was installed with turnaround experience and a pandemic took over the world that drastically changed the work environment. Today, WeWork is in a completely different business position and is worth a revisit with a fresh set of unbiased eyes.

WeWork has an ideal product for a post-pandemic world and strong normalized earnings that will be realized once occupancy recovers. With a more appropriate multiple to account for its high growth prospects, I believe the stock has at least 100% upside from current levels. In order for this to play out, WeWork only needs the economy to continue to reopen.

Demand Driven by Strong Coworking Tailwinds

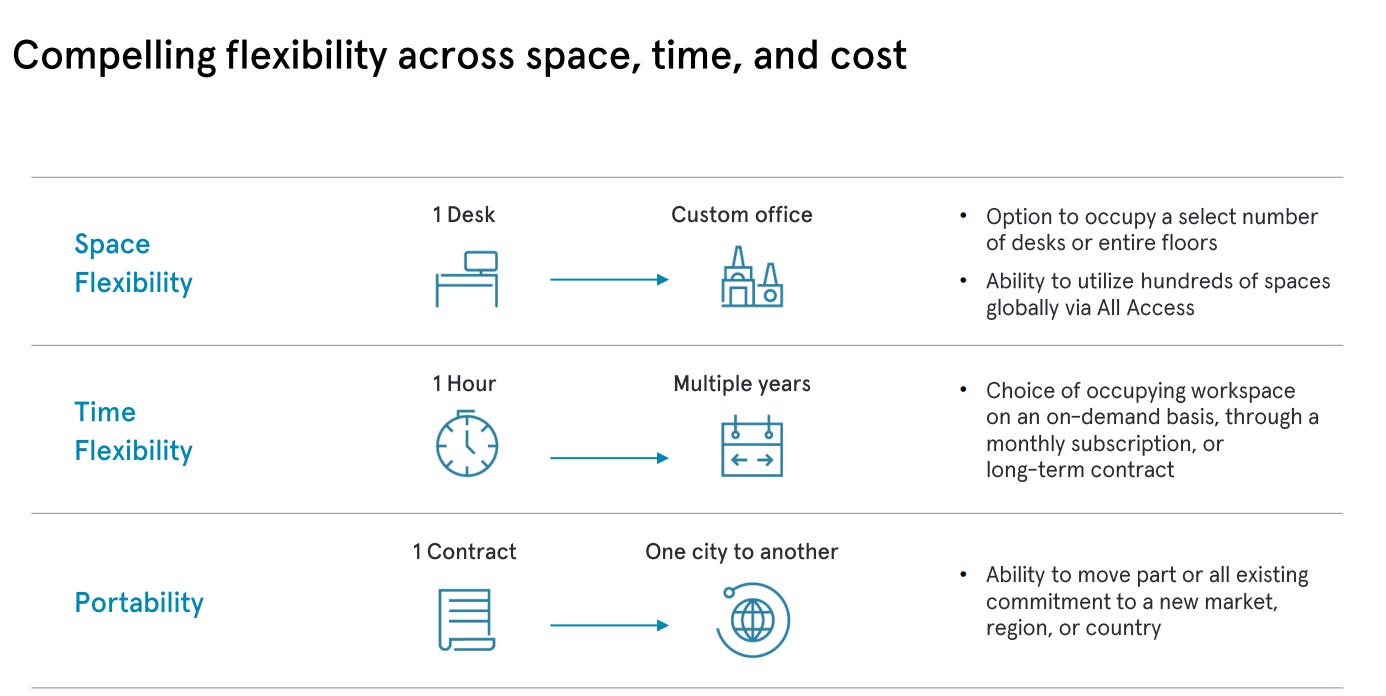

Coworking’s value proposition is primarily as a cheaper and more flexible work option for businesses compared to traditional commercial leases. Coworking offers flexibility on space (a dedicated desk, an office, or an entire floor), time (pay as you go, pay per month, or longer), and across geographies (in your hometown or when you’re traveling).

And on top of this, coworking is cheaper than the alternatives and offers a more vibrant work environment.

Naturally, the value proposition is even stronger in a post-pandemic world where uncertainty is high, workforces are fragmented across the country, and businesses are planning for hybrid work options with fluctuating office needs each day.

Said another way, if you’re a business (SMB or enterprise), would you rather sign a long-term lease and spend thousands to build out the office and get operations running, or would you rather sign up for a cheaper, built out coworking space with utilities and amenities provided, short-term leases, and the ability to scale up/down as your business changes?

This is a compelling product for businesses, and as a result, it’s not difficult to find forecasts that predict coworking will continue to grow and take share from traditional leases. WeWork highlights CBRE’s forecasts for coworking to grow to 13-22% of total office supply square footage by 2030, while FTI consulting forecasts 30% of total office supply.

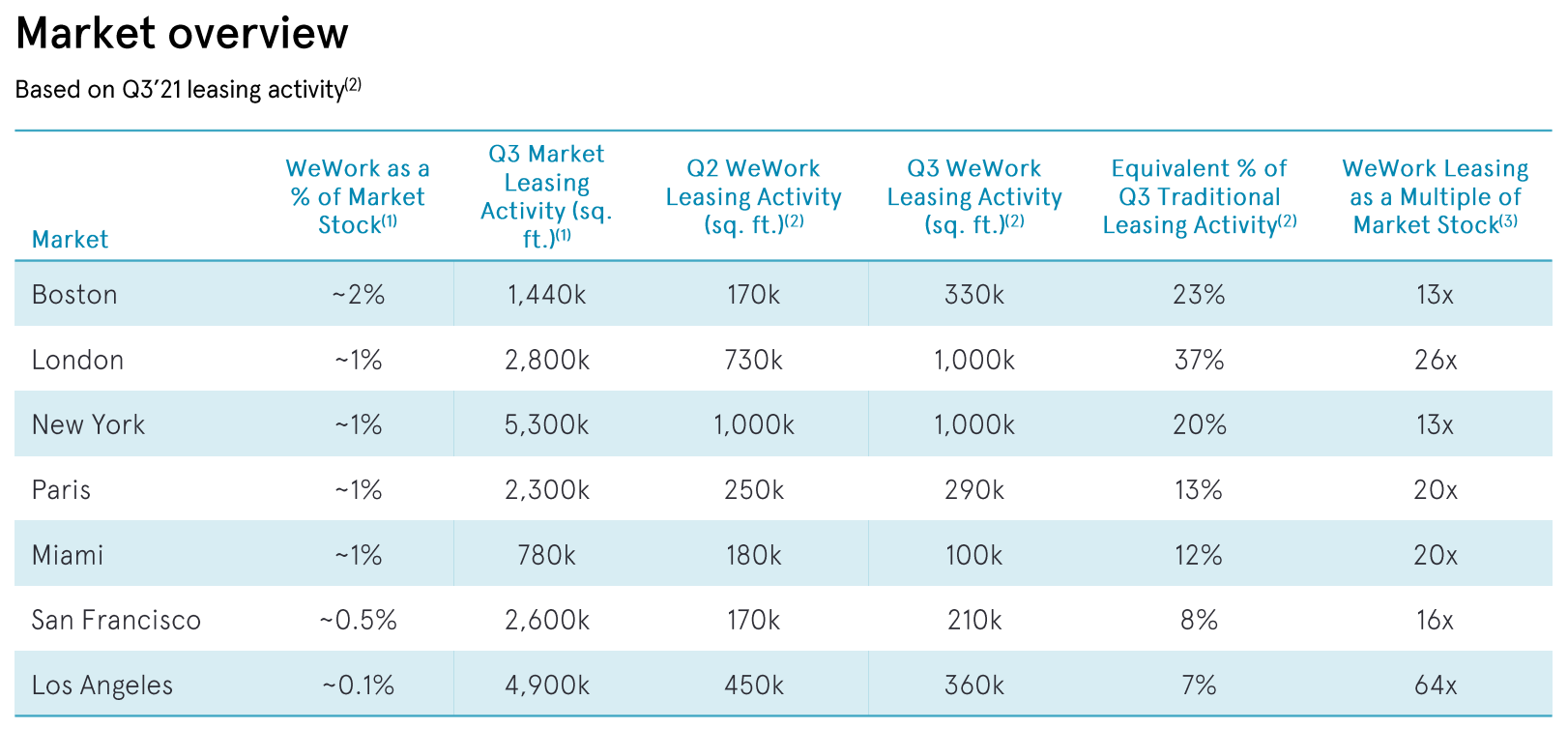

These forecasts are backed by results in 3Q21. WeWork highlights that while they have only ~1% or less of the total market office space in many of their major markets, they have been responsible for 10-40% of lease activity in those markets.

WeWork Competes with Scale and Premium Offering

Along with an attractive industry comes heavy competition. But with such strong long-term demand, I’d argue that there is more than enough space for numerous players to win within the industry.

With that said, WeWork is still well positioned to compete against the many other coworking players in the industry. While it admittedly doesn’t take much to open a coworking space, it does take a lot to build scale and have a large global footprint over time. As a result, there are only a handful of coworking spaces with over 100 locations. WeWork’s advantage here is scale - with almost 800 locations globally, the company can offer flexible options across the entire spectrum of offerings. Smaller players cannot offer the same value given their smaller footprints.

Additionally, WeWork competes in a different segment of the market than many other coworking spaces. WeWork offers a more modern and premium environment relative to competitors like IWG (the largest coworking space provider). Most of IWG’s spaces are priced lower, but feel outdated and are missing amenities (i.e. large open, shared spaces, modern interior design, larger kitchens, phone booths, glass walls). While this might not seem like much, this creates spaces that feel drastically different to customers (see IWG’s Regus below), and I believe the premium segment will gain share over time.

Regus - Little Rock, AR

WeWork - Plano, TX

Street Missing WeWork’s Massive Profit Potential

Once WeWork occupancy returns to prior levels, I project WeWork’s adjusted EBITDA margins to approach 22%. There’s a number of reasons for this surprisingly high level of profitability:

WeWork makes efficient use of its space in a number of ways. First, WeWork spaces are larger than most coworking spaces. In turn, WeWork has large shared spaces that feel welcoming, but are smaller as a percentage of the total building than competitors. Monetizable office sq. footage as a percentage of the total in turn is also higher.

Additionally, within that office space, WeWork has lower sq. footage per desk, enabled by a greater mix of 5+ person offices and other design decisions (i.e. narrow hallways). Larger offices carry tradeoffs - they are harder to fill, but once filled, have better economics with less sq. footage per desk. Customers of these offices are also more sticky. Ultimately, this means that WeWork is able to squeeze out more revenue per sq. foot than other coworking spaces.

Most of a coworking spaces’ costs are fixed or front-loaded. Rent alone makes up roughly 50% of EBITDA expenses, but stay flat as revenue grows (due to GAAP straight line amortizing). Advertising should also decline as locations approach full occupancy, offsetting other expenses. WeWork’s 2019 location contribution margins demonstrate the fixed nature of expenses as the location matures. Mature location contribution margins were 21% after 2 years.

It’s important to note that these location contribution margins were also from 2019, when the company’s expenses were drastically higher. Since that time, management has cut location expenses by $400M / sq. ft., cut SG&A expenses by $1.1 billion, and amended/exited 500 leases. Today, normalized location contribution margins likely look much better, which means even stronger operating leverage as occupancy recovers.

Recovering Occupancy to Send Stock Higher

The path to a higher stock is through higher occupancy and increased investor awareness of the story.

Occupancy rates today remain depressed, suppressing overall company revenue and profitability. Physical occupancy rate was 56% as of 3Q21.

Going forward, there’s still a risk that cases could spike again, in turn delaying office reopenings. This to me is the biggest risk to the story, but this time feels different. General public fatigue, rising vaccination rates, booster shot availability, vaccine approval for kids, and natural immunity all provide the foundation for a continued reopening and rebound in occupancy. And many employers plan to reopen their offices at the start of the new year. With higher occupancy will come massive leverage and higher profits, and a better understanding of the hidden value within the company.

Management believes the company will achieve breakeven adj. EBITDA in the first half of 2022 (with a roughly 70% occupancy as the breakeven point). Beyond that, the company sees 2023 revenue of $1.3 billion and adj. EBITDA margins of 22%.

Management Guidance As of 8/13/21

Using those targets, WeWork trades at just 6-7x 2023 adj. EBITDA. This compares to 1) EBITDA growth of roughly 50% in the following two years to 2025, and 2) hotels trading at 15-16x 2023 EBITDA, AirBnB trading at 50x with slightly lower growth, and Member Collective Group (Soho House) trading at roughly 20x with similar growth. Assuming a 20x multiple on WeWork’s 2023 estimates would imply a $30 stock. As the company begins to get closer to breakeven adj. EBITDA and demonstrates strong operating leverage, the street should begin to give WeWork more credit.

Beyond earnings, increased sellside coverage should also help increase investor awareness. WeWork recently went public via SPAC amidst many other companies going public and a mania around crypto assets. The sellside should begin to pick up coverage over the coming months.

🍌