Tesla: Expanding Auto Segments, Margins, and Multiples

Investors increasingly view the market as a bifurcation with long duration, hyper growth, and meme stocks on one end, and high quality and growth-at-a-reasonable price companies on the other.

There is a general perception among many investors that Tesla belongs in the hyper-growth/poopoo group. After all, it trades at 165x 2022 consensus GAAP earnings, is about to face heavy competition from legacy autos, is extremely volatile, and has a fanatic retail investor fanbase. Tesla must be frothy as well, right?

I argue that Tesla is actually more in the growth-at-a-reasonable-price group than one might think, and is likely to provide strong earnings growth (both near-term and longer-term) that will justify its high multiple and drive the stock higher, even after the recent run up in the stock.

The Playbook: Expanding Tesla’s Lead Into More Auto Segments

First, let’s establish Tesla’s revenue playbook. Tesla is currently the market share leader in the segments of the auto industry that it fully participates in - luxury sedans, CUVs, and SUVs in the US. Note that my definition of the auto industry includes ICE vehicles. Tesla’s focus is on extending this lead into more and more of the auto industry until it participates in every major vehicle, price point, and region in the world.

Tesla’s current market share lead within these segments is perhaps surprising or even unbelievable to many investors. The common arguments raised among bears and the media, in general, are that 1) Tesla’s total vehicle sales pale in comparison to legacy auto manufacturers, or 2) Tesla’s EV share is dropping in specific regions.

These points aren’t untrue, but they misrepresent Tesla’s position. Instead of using total vehicles across all segments (Tesla only participates in several segments currently), or looking at just EV share (which doesn’t capture EV share gains from ICE), or looking at country-specific market share within the EU (regions where they are more severely production constrained and without local production), I propose looking only at Tesla’s market share in the US versus all competing vehicles (including internal combustion engine vehicles) within the segments they participate in. Note that Tesla is still production constrained in the US, but less so than in other geographic regions. This is a more representative view of Tesla’s performance because they actually can better compete with product availability, and it’s more representative of the choices a consumer might face when considering a purchase.

This was the framework that I briefly touched on in my prior bullish post on Tesla in mid-2019, and a deeper dive into this view illustrates just how impressive Tesla’s performance has been since that time.

Note that I used entry level prices and goodcarbadcar’s definitions to help determine segmentation. S/X marketshare was calculated using 2020 data given that Tesla stopped production for the refresh for most of 2021, while 3/Y is calculated through 3Q21.

Looking at the data, Tesla’s market share was 32% for the Model S, 26% for the Model 3, 24% for the Model Y, and 17% for the Model X. These numbers are impressive not just for an EV manufacturer, but for all car manufacturers in general - across all vehicles, Toyota and Volkswagen lead the industry with just roughly 10% market share. Some other observations:

Model Y performance is extremely impressive considering that Tesla doesn’t currently offer an entry-level trim option (which puts the Model Y outside of the range of entry level prices in its segment and would disadvantage their volumes relative to competitors)

Model 3 volumes were probably being further constrained by the conversion of some production lines to Model Y in 2021, which limited production

Model X performance lagged Tesla’s performance in other segments but was still surprisingly the leader in full size SUVs. Elon has admitted several times that they made the Model X too complicated, and Tesla has taken these learnings to heart with vehicles introduced after the X (3, Y)

With such strong market share within existing segments, Tesla’s next steps are clear: make Tesla cars available in more segments and regions over time.

The immediate goal is to get production closer to demand levels for existing vehicles, as demand has outstripped supply for several years now, and expand into more regions. As stated earlier, Tesla will be opening another factory in Austin which will focus initially on Model Y production (thereby freeing up more production for the Model 3 as well at Fremont). Tesla will also expand geographically into Europe with its Berlin factory (both factories expected to begin production some time in 1Q22). With local sourcing and production in EU (where Tesla is currently passing on a 10% import tax), Tesla can better compete by offering better pricing and improved logistic costs. Eventually, Tesla will also introduce the entry-level Model Y, unlocking a new segment within CUVs.

In terms of vehicles, Tesla will look to introduce the Cybertruck, Semi, and Roadster in the coming years, and a high-volume $25K vehicle beyond that. If they’re able to maintain at least a 20% market share in other segments as they expand, Tesla would be on its way to achieving 20M vehicles longer-term.

Competition Will Eventually Come - Can Tesla Maintain Market Share When It Does?

The major question that jumps out from the above charts: why has Tesla done so well in these segments? The answer to this question carries implications for how sustainable Tesla’s lead is, especially as new EVs come to market. Is it simply because people want electric vehicles, and Tesla models are readily available? Or is there some other sustainable moat that will allow Tesla to maintain share in the face of upcoming competition?

My own view in brief is that Tesla’s advantage, broken out into its components, lies in its strong engineering and product specs, the supercharger network, seamless integration between hardware and software, autonomy features, manufacturing, access to batteries, and vertical integration.

More succinctly though, Tesla’s advantage lies in the overall user experience (which requires all of the above advantages). While I’m hesitant to roll out the analogy to Apple (the world doesn’t need anymore of these), I do believe that Tesla’s advantage is very similar to Apple’s advantage over competitor phones. Many investors have noted Apple’s ecosystem and network effect as a moat, but my own belief is that Apple’s sustained success is primarily due to the entirety of the user experience, which is just smoother and more intuitive than competitors’. Other competitor phones work just fine - they’re functionally very similar to Apple’s capabilities, probably screen even better on paper, and have all the apps you’ll need. But they don’t have the overall customer experience that a vertically integrated company like Apple does. I believe Tesla vehicles have high NPS and customer satisfaction scores not because of electric vehicle-specific traits (fast acceleration, or the “green” halo) but because of a similar magical user experience that starts with the ordering process on the website, and extends into taking delivery (often at your house), simple Superchargers, and a more familiar interior UI for many phone-loving consumers.

Whether it’s because of tech debt and legacy systems, or old-fashioned senior management, or their history of outsourcing so many elements of the user experience to other companies, legacy auto companies have really struggled to create intuitive user experiences. To name a small but seemingly frustrating example, numerous Ford Mach E customer reviews have noted the difficulties in finding chargers while on a long-distance route within the UI.

Legacy companies face the same difficulties in creating great user experiences in other industries as well. Newer companies, like Carvana, Opendoor, Netflix, Robinhood, or Uber (to say nothing of their financials), have been able to gain significant share from legacy incumbents simply by focusing on this weak spot. And while newer EV entrants like Rivian or Lucid might not struggle as much, they still face manufacturing difficulties that only Tesla (among the new EV startups) so far has been able to get over.

Tesla’s moat is in their ability to combine many of the above-listed advantages and vertical integration into one seamless user experience. While legacy auto might be able to create EVs with close-enough specs over time, I’m skeptical of their ability to create the entire magical user experience for customers.

Industry-Leading Margins to Continue Expanding

Tesla combines strong topline prospects with an industry-leading margin profile that is likely to continue to expand. During Tesla’s meteoric rise over the last several years, Sanford Bernstein analyst Toni Sacconaghi often noted that in order to justify Tesla’s valuation, one had to believe that they would achieve industry-leading volumes along with margins on par with the leaders in the space (high single - low double digits). This would represent a difficult balancing act, as Tesla has historically struggled to generate strong profitability while selling very expensive cars, and industry-high volumes would require lower price points, which naturally carry lower margins.

Now, it’s increasingly looking likely that Tesla will not only achieve industry-leading margins while selling luxury vehicles, but that they will blow prior industry highs out of the water as they continue to scale and gain share from the rest of the broader auto market. Tesla achieved an industry-leading GAAP operating margin of 14.6% in 3Q21 (or 11.1% over last four quarters), despite:

Operating a jam-packed factory in one of the more expensive production areas in the world (Fremont) and operating another factory that continues to ramp in production (Shanghai)

Not producing any of its highest margin vehicles in 3Q (S/X)

Incurring some of the costs for its two new factories without any of the volume benefit

Incurring expenses to cover for supply chain issues

Operating below full capacity due to supply chain issues

Being burdened by an energy business that is battery-starved and fully loaded with expenses

For context, legacy auto manufacturers (Toyota, Volkswagen, GM, Ford, Daimler, BMW, Honda, Hyundai, and Nissan) have averaged 4% GAAP operating margins from 2017 to 2019, and posted similar levels last quarter. Daimler and BMW have posted the highest GAAP margins in recent history with 9% operating margins in 2017.

Going forward, management has noted that they believe operating margins are likely to continue to expand over time from the 14% last quarter. It’s difficult to see why they wouldn’t. Many of the issues noted above will reverse, as Tesla’s two new factories in Texas and Germany will begin to ramp production in 1H22, production will continue to grow at their existing Fremont and Shanghai factories (as they did in 4Q21), ASPs will get support from recent price increases, supply chain issues should ease, and high margin X/S sales should return. Additionally, Tesla’s 4680 batteries (which are targeted to get into production vehicles some time in 2022, potentially in the first half) have the potential to drastically lower costs while also easing battery constraints on production, and Tesla’s other manufacturing innovations remain underway (structural battery pack and front/rear castings). The biggest headwind they will face is factory opening expenses in the coming quarters, but this headwind appears manageable and likely to be offset by the numerous tailwinds over time.

Longer-term, a key question will be where margins end up as Tesla begins to move down into lower-priced segments. Visibility here is somewhat limited, but Tesla’s current margin profile bodes well (several points higher than other volume luxury manufacturers), and the manufacturing innovations underway provide a roadmap to introducing lower priced EVs while maintaining strong margins.

The key underpinnings of Tesla’s margin sustainability is tied to 1) Tesla’s pricing power driven by its strong brand and products, 2) their engineering, manufacturing, and software advantage, especially within electric vehicle production (which is increasingly looking like a different-enough process than just manufacturing ICE vehicles), and 3) their ability to secure battery capacity for higher production volumes. These are durable advantages that will be difficult to catch up to by both legacy manufacturers and newer EV startups.

Valuation Is More Reasonable Than It Appears

One of the most common criticisms about Tesla, even among neutral observers, is its high valuation. I believe many investors arrive at this conclusion by looking at valuation metrics automatically calculated by Bloomberg, FactSet, or CapIQ, which use consensus estimates. The issue is that consensus has been consistently and utterly wrong on Tesla.

A quick glance at estimates for the just-reported 4Q21 deliveries number illustrates their inaccuracy. The actual 309K delivery print was well-above consensus of 267K, but the inaccuracy was greater than this the further you go back in time. A year ago, consensus was at 227K, and two years ago you’ll see an even worse delta at 172K.

Even greater inaccuracies are seen on GAAP operating profit estimates. Today’s 2021 consensus estimates (which will likely still be too conservative once 4Q is reported) sit at $6.2 billion, but two years ago was $2.6 billion. Back then, Tesla probably looked expensive on $2.6 billion of EBIT estimates, but ended up at an inexpensive multiple off of $6.2 billion of EBIT.

The moral of the story is that you’ve got to do the work and model out your own numbers on Tesla before you jump to conclusions on the company’s valuation. This is generally true for many companies out there, but it’s even more true for a controversial stock like Tesla where the range of possible estimates can vary so greatly. Naturally, if you’re negative on Tesla already, you’ll likely end up even lower than consensus and an even more expensive valuation. But for those without a strong opinion on the name, I would highly encourage you to ignore valuation based on consensus numbers and model out your own estimates.

My own 2022 GAAP EPS estimates for Tesla stand at roughly $11 (vs. current 1/2/22 consensus of $7.28), predicated on 1.6 million of deliveries and a 18% operating margin. A closer look at my simplified model and estimates can be found at my site, where you can also plug in your own assumptions and estimates to tie to valuation.

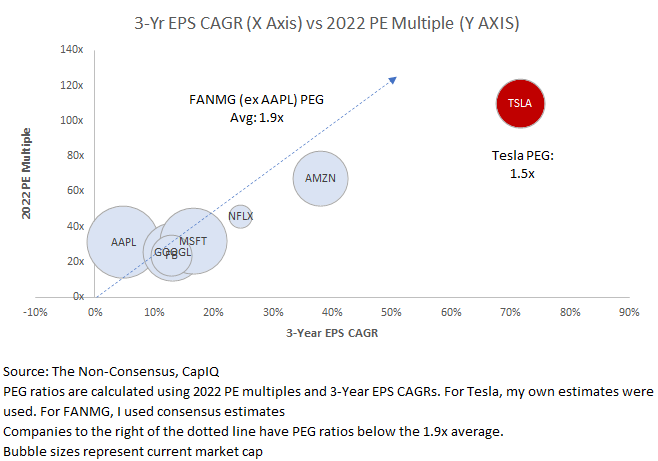

Using my 2022 estimates, Tesla trades at a 106x PE multiple. While this still might seem high to some, I would argue that this is in fact low when considering future growth and large-cap tech comps. On average, FANMG (Facebook, Amazon, Netflix, Microsoft, and Google; Apple was excluded as their PEG ratio skews the average too favorably for Tesla) PEG ratios currently sit at 1.9x. In other words, investors are willing to assign a 2022 multiple roughly 2x higher than projected 3-year EPS growth forecasts for large cap tech. For Tesla, its PEG ratio stands at 1.5x (using my 3-year growth forecast of 72%). Assigning Tesla a PEG ratio more in line with large cap tech would imply a PE multiple of about 135x. This would then translate into a $1,500 target price off of my 2022 EPS estimate, or roughly 25% upside from the 1/3/22 stock price. Further upside exists as my numbers may still end up being conservative, particularly on margins, but I’ll revisit these numbers over time as we get more datapoints.

The key to remember here is that 1) investors are willing to pay elevated multiples if growth is high and there is sufficient visibility to that growth, and 2) Tesla’s consensus numbers have been consistently too low. Tesla also offers other benefits that other large cap tech doesn’t, including ESG-related themes and upside optionality (on autonomy and the energy business) that justify higher multiples.

Path to Higher Stock is Through Expansion in Auto Segments, Margins, and Multiples

Tesla’s path to a higher stock is simple. First, Tesla will extend their strong market share into more auto segments and regions through vehicle launches and international factory openings. Second, margins will continue to expand through increased production and continued manufacturing innovations underway, potentially going north of 20% longer-term. Third, the street will continue to revise estimates and multiples higher as investors give Tesla more credit for its strong growth and execution. These pieces should ultimately lead to a higher stock over time.